Esta evolución puede ser una revolución.

Get this executive brief in pdf format

The first offshore wind turbine that was installed in 1991 in Denmark marked the beginning of a new era. Almost 30 years later, the sector is reaching full maturity with more than 50 GW installed. But the installed offshore wind turbines have a limit, that of the depth of water which must remain below 50-60 m. To overcome bathymetry, it is necessary to use "floating" foundations, a new frontier of the sector. In the same dynamic, offshore wind energy is leaving its historical development area, Europe, to enhance new geographies such as the United States or Asia. These not only experience bathymetric conditions, but also climatic conditions different to Europe’s that are sometimes extreme, such as cyclones.

Floating offshore wind: a rapidly expanding niche

The world's first floating wind turbine was installed in 2009 at a depth of 200 m about 10 km off the coast of southern Norway. Siemens supplied the 2 MW wind turbine and Technip oversaw the construction and installation of the floating foundation for the client Equinor (Statoil at the time). The cost of this project was about € 50 million. 10 years later, this wind turbine is still producing electricity, but Equinor has sold it to Unitech Offshore AS who will use it to test a new cable/connection system.

In 2017, Hywind Scotland’s first industrial scale offshore wind project started production. The overall investment was announced at around NOK 2 billion (200 M€), with Equinor as the main investor and Masdar holding 25% of the project. The 30 MW capacity is spread over six 5 MW wind turbines located off the coast of Peterhead at a water depth of around 100 m. The project is still the most productive offshore wind project in the world, with a record load factor of 57% measured in 2020.

The world's third and fourth floating wind projects were installed in 2020 and 2021. These are Windfloat Atlantic led by a consortium composed of EDPR, Repsol, Engie and Principal Power (who supply the floaters technology) with a capacity of 30 MW installed off the coast of Portugal at a depth of about 100 m, and the Kinckadine project of 50 MW, led by the company COBRA installed in Scotland off the coast of Aberdeen roughly at the same water depth. It should be noted that Windfloat Atlantic is the first project to claim "external" financing via the participation of the European Investment Bank (EIB). Finally, the largest floating wind project with an installed capacity of 90 MW in Norway has just produced its first electrons. It has the particularity of supplying electricity to Snorre and Gullfaks oil platforms in the North Sea. The wind turbines’ floating foundations water depth is also a first at nearly 400 m deep.

In total, approximately 200 MW of floating wind projects have been installed to date. The acceleration of construction projects should continue in France, that has big long-term ambitions for this technology (E. Macron announced that by 2050, 20 GW of the 40 GW of offshore wind projects will have to be floating), and should see three projects of about 30 MW on its Mediterranean coast in the near future. These "experimental" projects, installed in about 100 m of water depth, were launched following a call for expressions of interest from ADEME in 2016:

- the Eolmed project led by Qair, Total Energies and BW Ideol (the supplier of the project's floaters technology) located in Occitanie;

- the "Floating Wind Turbines of the Lion Wind" project led by Engie and EDPR using floaters technology implemented on WindFloat Atlantic.

- and finally, the "Provence Grand Large" project led by EDF EN using an innovative floater technology developed by SBM Offshore.

The fourth project that was part of the same call for expressions of interest from ADEME was located on the Atlantic coast, using the Naval group floater technology developed by Shell, and has just been abandoned. All those projects benefited from EIB financing and the establishment of non-recourse financing traditionally used on fixed offshore wind projects.

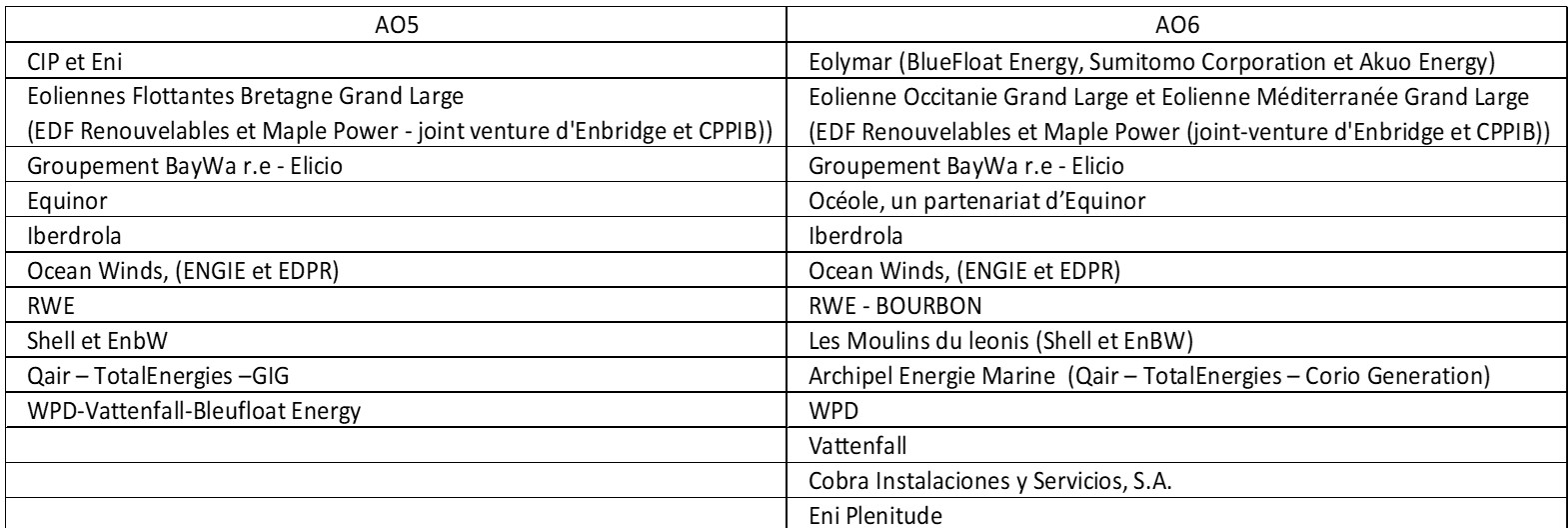

In line with these developments, France launched the first calls for commercial projects of 250 MW in the Atlantic and 2X250 MW in the Mediterranean area for commissioning in 2029. This call met with great success, with at least 10 consortia shortlisted for the competition. The list of these consortia is given in Table 1 below.

Table 1: List of pre-qualified consortia for calls for offshore wind projects in France

Source: AO5 for the Atlantic Sea and AO6 for the Mediterranean Sea

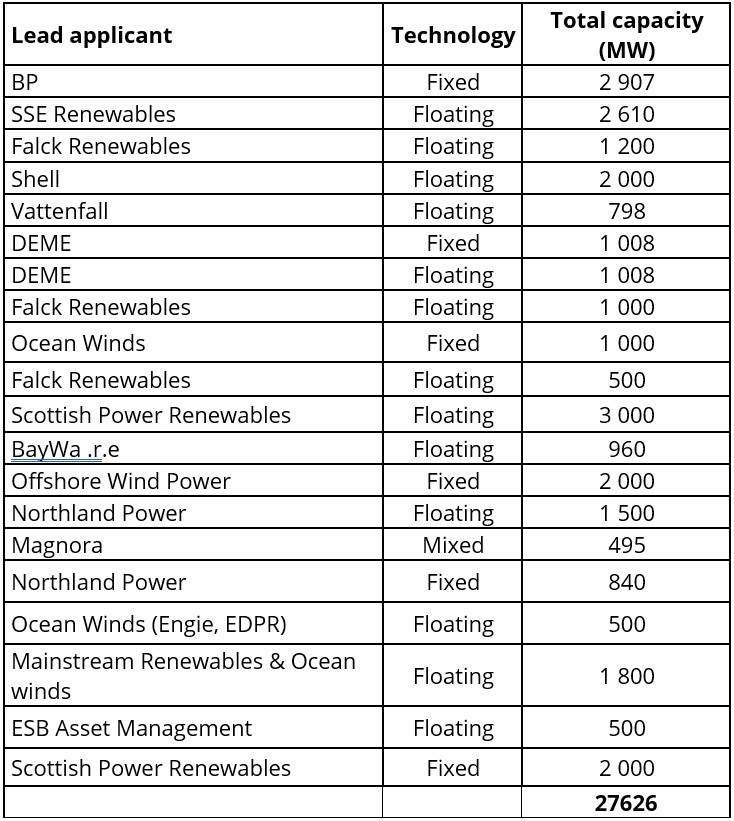

Scotland left its mark on the sector by organising the selection of consortiums for more than 27 GW of offshore wind power, including 17 GW using floating foundations. As in France, the success of this public solicitation was significant with the participation of 74 consortia’s in the selection procedure. The list of winners finally selected is given below (Table 2).

Table 2: List of winners selected for the concession of the development of the area in Scotland

Source: Scotwind

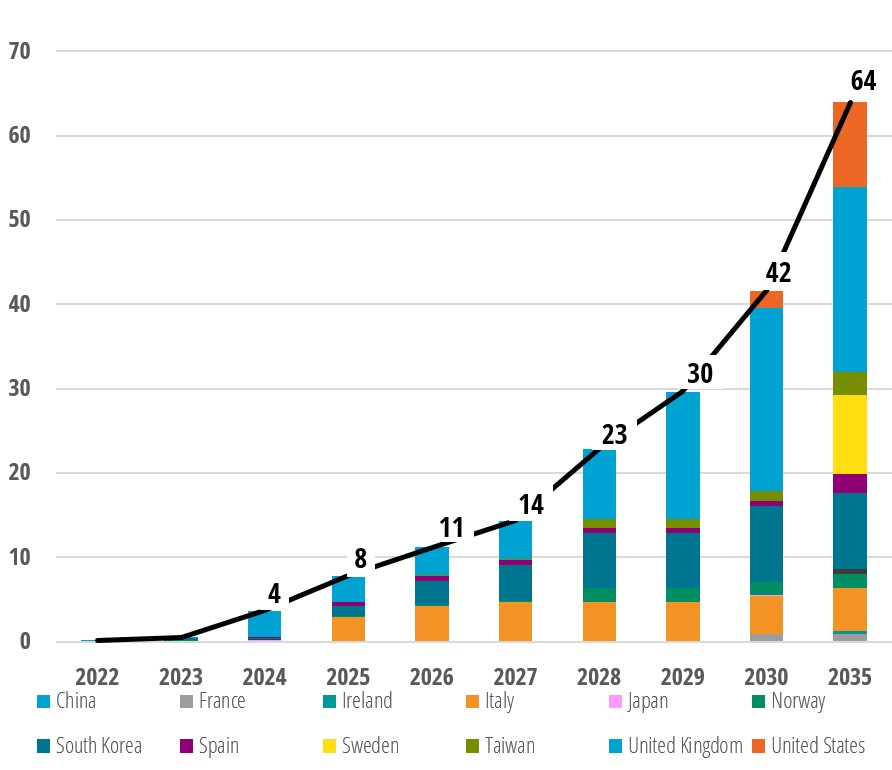

Finally, in the latest announcements that have marked the floating wind sector, it is necessary to mention the Biden administration which brings the United States into the competition. At the beginning of September 2022, it was announced that15 GW of floating wind projects were planned for 2035, and in December 2022, the winning bidders of the first lease sale were announced for a total area with a potential of around 5 GW. Asia is also a promised land of floating wind power with particularly active countries such as South Korea, Japan, China, Taiwan, and the Philippines.... The main areas of floating wind energy development in the world are recalled in Figure 1 below.

Figure 1: Major offshore wind developers

Source: Global Wind Energy Council – Global Offshore Wind Report 2020

As a symbol of the current dynamic of the floating offshore wind sector, the GWEC (Global Wind Energy Council), has revised its long-term outlook: they have multiplied by 4 the figures published between 2020 and 2022, to reach nearly 28 GW in 2031. Enerdata forecasts are slightly more optimistic, with 42 GW of projects in the pipeline that would potentially be installed by 2030, and up to 64 GW by 2035.

Floating offshore projects could thus account for more than 20% of all offshore projects globally installed by 2030.

Figure 2: Evolution of cumulative floating offshore wind projects1 around the world - GW

Source: Enerdata, Power Plant Tracker

In connection with the development of these new areas, the appearance of the T-class for Typhoons machines capable of withstanding winds above 257 km/h. Wind turbine manufacturers have adapted standards and technologies.

Typologies of actors

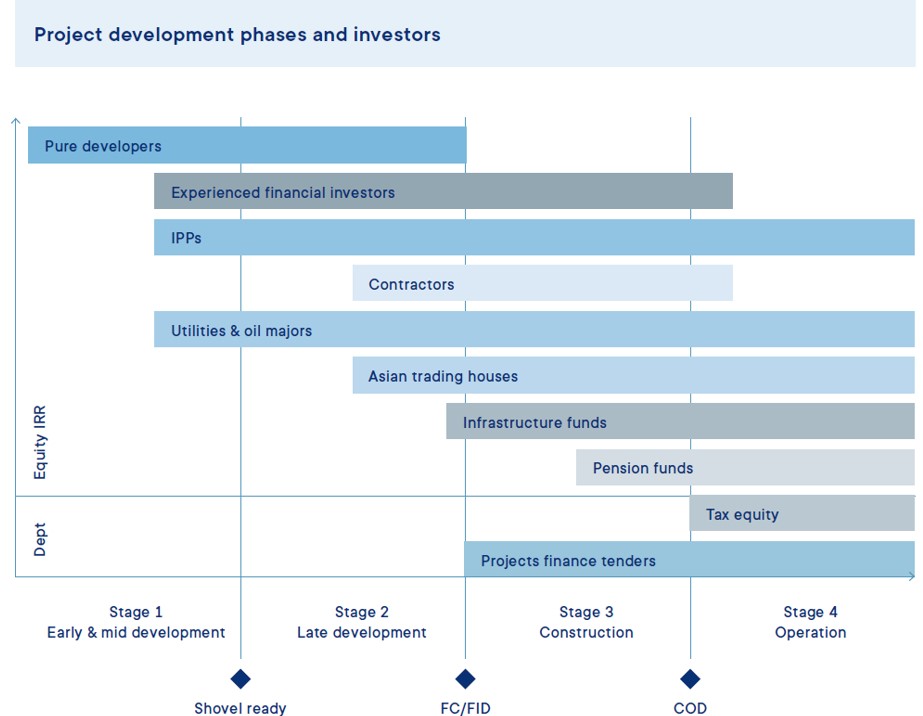

The actors involved in the development of floating wind projects are very varied, as can be seen in Tables 1 and 2 above. They consist of developers of renewable energy projects (Akuo Energie, Qair, Baywa r.e., ...), and, more surprisingly, EPC contractors / builders of offshore wind projects (DEME, COBRA,...) who see an opportunity to diversify their risks. There are also the large historical "utilities" (EDF, Iberdrola, RWE, Vattenfall,...) who are more comfortable managing these large-scale projects rather than multiple small solar or wind projects, and financial players who sometimes specialize in offshore wind (Bluefloat Energy (Quantum Energy), the Caisse des Dépôts et Consignation, Green Investment Group and the Canada Pension Plan Investment Board (CPPIB) involved via Mapple Power, ...). Finally, there are also oil groups seeking to leverage their know-how in offshore O&G such as Shell, BP, Total Energies or Enbrigde. These actors are not necessarily involved in the same phases of project development as shown in Figure 3 below.

Figure 3: Typology of factors involved in offshore wind projects according to the maturity phases of the projects

Source: Guillet, Financing Offshore Wind 2022

Technology

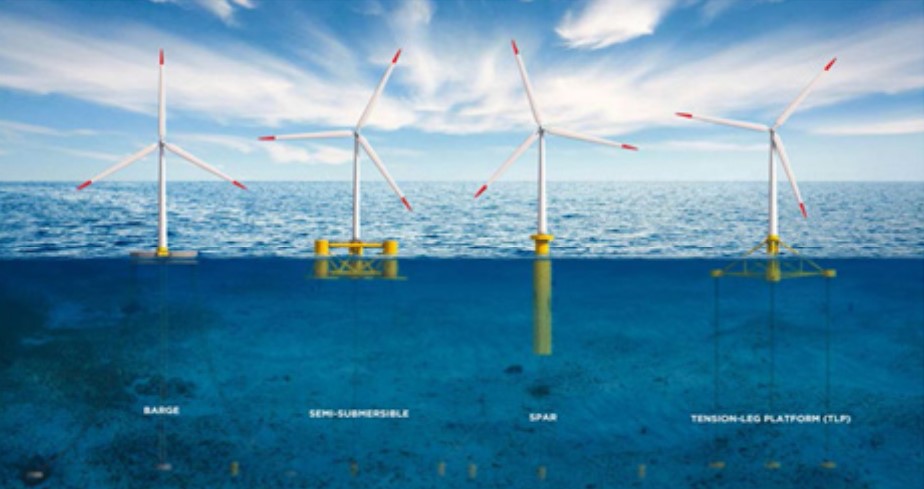

The wind turbines used in floating projects are exactly the same as those used in bottom fixed offshore wind projects. There are no wind turbine technologies dedicated to commercialised floating wind markets (there are some ongoing R&D projects). The essential difference between the two forms of offshore wind projects (floating and bottom fixed) stems from the nature of the foundation. There are 4 main types of floating wind turbine foundations as shown in Figure 2 below.

Figure 4: Types of technologies

Source: GWEC, Report 2022 – Floating Offshore Wind – A global opportunity

These concepts come largely from the gas industry. These are:

- barge foundation, typically technology developed by the French company Ideol, tested off the island of Groix in France;

- semi-submersible foundation, a structure that floats between two "canisters" connected to each other by a metal mesh. This is the technology used by the Windfloat Atlantic project and developed by Principle Power. There are two options for this technology. One is active in which ballasts filled with water permanently to ensure the stability of the structure, and the other is passive, without ballast;

- SPAR foundation, a “pencil” buoy with a large draft (up to 100 m), developed by Equinor in its Hywind projects;

- "Tension Leg Platform" (TLP), a technology whose float stability is ensured by tendons anchored to the seabed. This technology is developed by SBM Offshore and will be installed off the coast of Fos-sur-Mer in France as part of a demonstration project led by EDF EN.

Each of these structures can be made of concrete or steel. The choice of material depends on the location of the site, the potential effects of scales, the technical capacity of the operators / contractors selected, the need for local jobs and so on. Globally, the majority of projects are based on steel solutions.

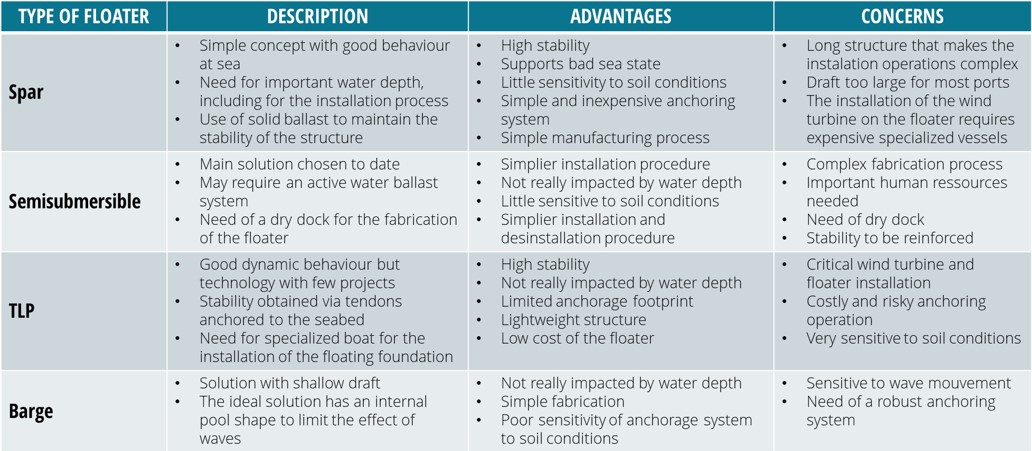

The disadvantages and advantages of each of the proposed floating foundations are given in Table 3 below. Overall, the most popular technology is the semi-submersible float.

Table 3: Advantage/concerns of different types of floaters

Source: GWEC, Report 2022 – Floating Offshore Wind – A global opportunity, and author

Transport and transmission of electricity

People imagine that floating offshore wind projects are by nature installed far from the shore. In fact, even bottom fixed offshore wind projects may be installed more than 100 kms from the shore. This is the case for the EnBW 600 MW Albatros project in Germany and England where the development project is installed in the Dogger bank zone that is 100 to 200 km from the shore. One important limitation of floating / bottom fixed offshore wind projects that are far from shore is transmission losses, these can be kept to a minimum by using DC substations rather than AC. Floating offshore projects need to use dynamic cables. As of today, most floating offshore wind projects are installed at a 100 m depth which doesn’t require dynamic cables. But for projects installed in deeper water, inter-array dynamic cables, and dynamic cables to export to the shore will be required.

Costs

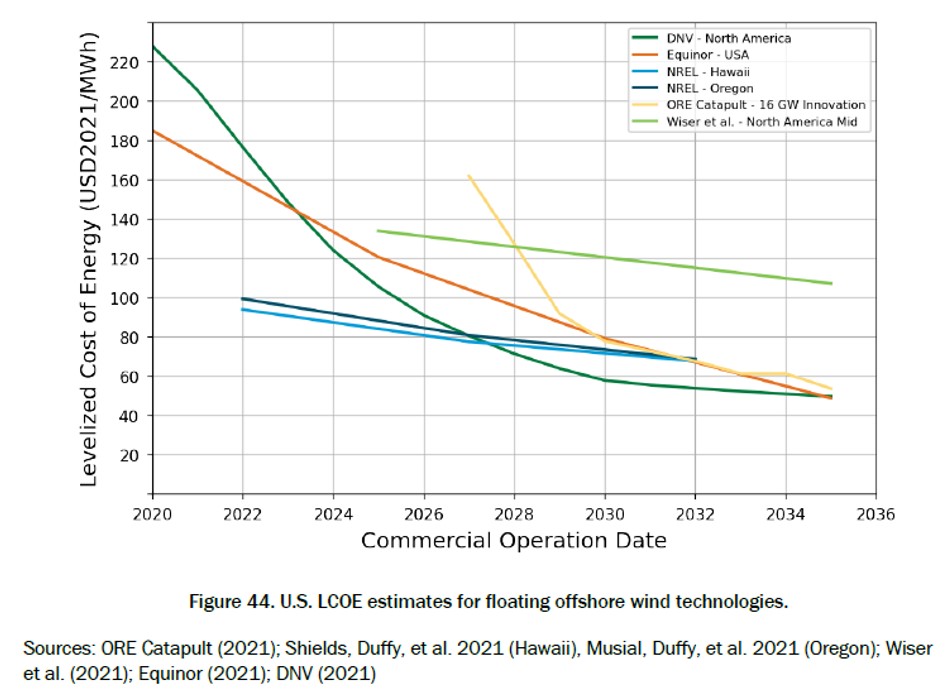

The costs of electricity produced by floating offshore wind power are now around €150 to €200 / MWh for projects in operation. But with the expected increase in capacity, it is anticipated that the cost of electricity production will fall sharply. As a symbol of these expectations, the ceilings imposed on calls for tenders in France being between 110 and 120 € / MWh. Costs are expected to continue to fall in the future and approach those observed on bottom fixed offshore wind globally between €50 / MWh and €100 / MWh. For example, the US floating wind program was launched in early September with the objective of reducing costs by 70% to reach a target of $45 / MWh by 2035. The expected evolution of costs in the wind energy sector is recalled in Figure 4 below.

Figure 5: Reduced costs in the floating wind sector

Source: Musial, et al., Offshore Wind Market Report: 2022 Edition

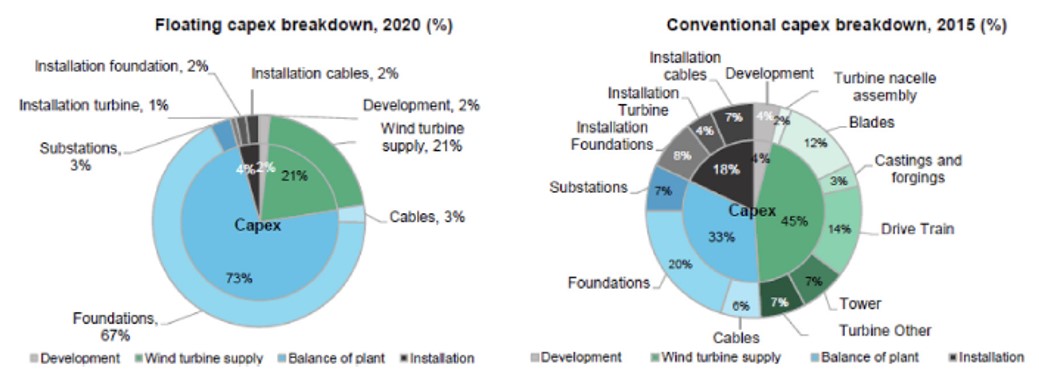

Costs will depend on the characteristics of the sites on which the wind turbines will be installed, the floater technology chosen, the effects of scales, and so on. It should also be noted that the capital expenditures (CapEx) of a floating offshore wind project are different from that of a bottom fixed offshore wind one, with a lighter wind turbine weight (see Figure 5 below).

Figure 6: Comparison of the CapEx composition between a fixed wind project and a floating wind turbine

Source: Kausche, Adam, Dahlhaus, & Großmann, Floating offshore wind - Economic and ecological challenges of a TLP, 2018

It should be noted that floating offshore wind projects avoid a critical construction phase of bottom fixed offshore wind projects, namely the offshore assembly of the wind turbine and its foundation at sea, which are both risky and expensive activities. A floating offshore wind turbine and its foundation are usually assembled shore-to-dock, in a protected environment, then towed to their final location. These activities require vessels that are much simpler and much less sensitive to weather conditions than those used for bottom fixed offshore wind projects.

In terms of financing, the floating wind industry is currently where the fixed wind industry found itself fifteen years ago. Both technologies are capital intensive with low operating costs. The final cost of electricity generated by these projects is thus largely determined not only by the level of investment required by the project, but also by the cost of financing, Over time, the bottom fixed wind sector has managed to limit the use of equity and make extensive use of high levels of debt. The floating wind sector will have to prove its ability to manage risks well enough if it is to use the same types of financial mechanisms that have proven effective for the bottom fixed sector, with debt levels of up to 80% of the required funding levels.

Environmental impact

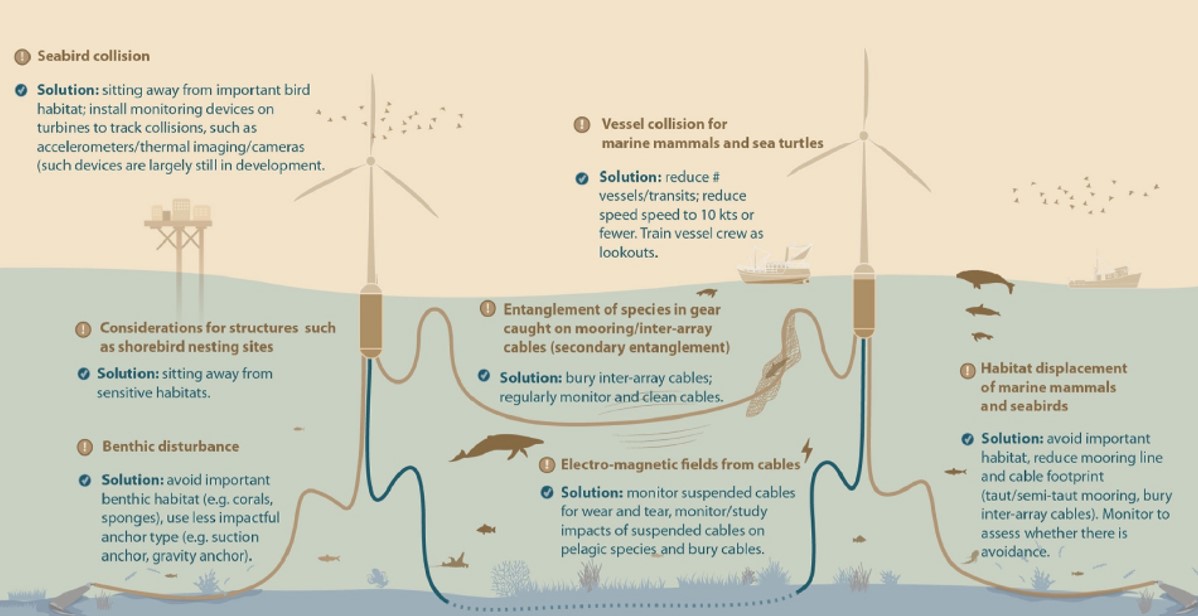

Like all heavy infrastructure projects, floating offshore wind projects impact the environment. The most scrutinized is probably that of its ability to produce electricity with a low level of greenhouse gas emissions. As the floating wind sector is in the infancy of its history, there is relatively little data. Nevertheless, ADEME in France carried out a study of the 30 MW pilot projects being installed in the Mediterranean sea, and found they produced an average of around 37.5 grams of CO2 equivalent/KWh, which is quite low (onshore and bottom fixed offshore wind sectors produce around 15 grams of CO2 eq/KWh compared to between 25 to 44 g CO2 eq/KWh for solar PV). This type of project will also generate other environmental impacts which are summarized in Figure 6 below.

Figure 7: Environmental impact of floating offshore wind projects

Source: Maxwell, Kershaw, Locke, & Conners, Potential impacts of floating wind turbine technology for marine species, 2022

Floating and bottom fixed offshore wind projects have similar impacts on the environment. The effect of turbine blades on birds is the same, but the other impacts may have different forms. During the construction phase, floating wind projects will probably have a lower impact on the environment because the anchoring systems are less aggressive, especially on noise levels, with no foundation "pounded in the ground" by hydraulic hammer as can be the case for bottom fixed offshore wind projects. However, during their operational phase, the risks of lost and drifting fishing nets clinging to the anchoring systems may need special monitoring actions.

Key take-aways

- Floating offshore wind is the next growth driver of the offshore wind sector with 42 GW currently in project and expected by 2030, i.e. more than 20% of all offshore wind projects

- This new technology breaks free from water depth restrictions and allows massive production of renewable energy in new areas outside Europe, the historical region of bottom fixed offshore wind developments

- Many different types of players are active in the development of this intensely competitive and dynamic emerging sector

- The expected costs of electricity produced by floating wind projects should be close to those of bottom fixed offshore wind projects, around €50 to €100/MWh

- Given the scale of the projects envisaged, a duty of vigilance is required on the impact on the environment linked to the implementation of large-scale floating offshore wind projects

References

- Global Wind Energy Council. (2022). Floating Offshore Wind – a Global Opportunity.

- Guillet, J. (2022). Financing Offshore Wind. Hamburg: World Forum Offshore Wind.

- GWEC. (2021, Septembre 9). Global Offshore Wind Report. Bruxelles, Belgique.

- Kausche, M., Adam, F., Dahlhaus, F., & Großmann, J. (2018, March 23rd). Floating offshore wind - Economic and ecological challenges of a TLP. Renewable Energy, pp. 270-280.

- Maxwell, S. M., Kershaw, F., Locke, C. C., & Conners, M. G. (2022, January 25th). Potential impacts of floating wind turbine technology for marine species. Journal of Environmental Management.

- Musial, W., Spitsen, P., Duffy, P., Beiter, P. B., Marquis, M., Hammond, R., & Shields, M. (2022). Offshore Wind Market Report: 2022 Edition. National Renewable Energy Laboratory.

About the author

Stéphane His

Senior Energy & Climate expert

Stephane is a climate and energy consultant since 2020 and has been working in this field for the last 25 years.

He started its carriers at IFP EN in 1996, being responsible for “well to wheel analysis” and long term prospective in the transport sector in France. In 2008, he became VP renewable energies at Technip where he developed the dedicated to offshore wind business unit. In 2016, he joined the AFD and hold there the senior mitigation climate expert position.

With Enerdata, Stephane has been collaborating in the offshore wind sector for a industrial French client as well as to analyze oil and gas supermajor decarbonization strategy. He holds a HEC master is an engineer specialized in thermic and energetics from the university of Compiègne (UTC).

Notes:

1 Figures only reflect current projects and don’t include project announcements that have not gone through or are at very early stages of development.