Dynamics and Challenges Following Russia’s Invasion of Ukraine

Get this executive brief in pdf format

Russia's invasion of Ukraine in February 2022 reignited debates in Europe and the United States on the dependence of nuclear industries on Russian uranium fuel supplies. These discussions have intensified with the inability, in Washington and Brussels, to impose sanctions on Russian companies in this sector until now. Simultaneously, the amplification of extreme climatic events and the rise in energy prices have revived policies for the construction of nuclear power plants. While Russian industry, centralised within the Rosatom group, holds leadership in exports of nuclear technologies and services, concerns are being raised about Moscow's ability to use this position and context for geopolitical purposes.

Uranium enrichment remains a mandatory step for supplying the world's nuclear parks and will remain so until the end of the century, in the light of power plants currently in operation and under construction. In addition, the geopolitical dynamics of enrichment supersede those of the preliminary stages (the extraction of natural uranium and its conversion) and the following stages (fuel assembly). This brief will be structured around a several key questions: what is the current and future state of nuclear energy in the world? What is uranium enrichment? How did Russia come to dominate the sector? What are the impacts of the war in Ukraine on the sector? Which new actors could emerge? And apart from Russia, what major challenges remain, and what solutions exist?

The current and future state of nuclear energy

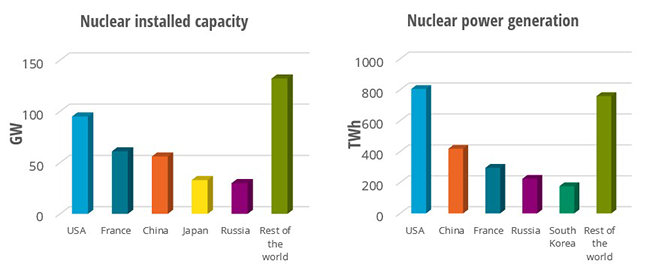

Uranium enrichment is essential for supplying nuclear power plants, which have become of vital part of many countries’ power supply and energy strategy. According to Enerdata, as of end 2022, nuclear represented about 5% of the world’s installed capacity with 407 GW. The United States is the country with the most installed nuclear capacity with nearly 95 GW, followed by France (61 GW), China (56 GW), Japan (33 GW) and Russia (30 GW). As of March 2024, 85 GW of nuclear capacity was under construction (with 31 GW in China alone) and 354 GW was under development (including 174 GW in China). In terms of power generation, nuclear represented 9% of worldwide electricity production with 2,677 TWh (2022). The United States produced the most power from nuclear in 2022 (805 TWh), followed by China (418 TWh), France (295 TWh), Russia (224 TWh) and South Korea (176 TWh).

Figure 1: Nuclear installed capacity and power generation by country (2022)

Source:Enerdata, Global Energy and CO2 data

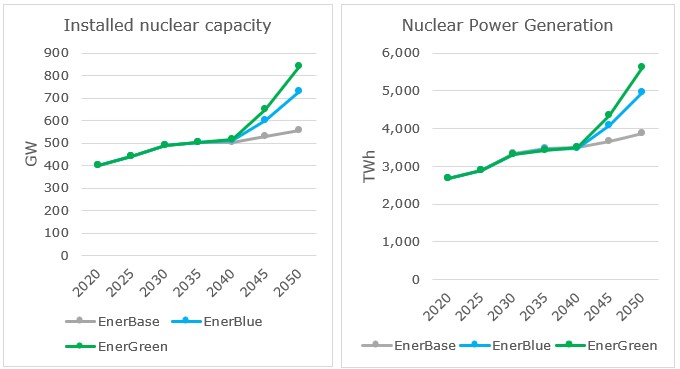

Enerdata’s EnerFuture outlook outlines three scenarios on the evolution of nuclear capacities and production to 20501. Under the baseline scenario (EnerBase), nuclear capacities and power generation would reach 558 GW and 3,862 TWh, respectively, by 2050. Under a second scenario, in which countries would achieve their previously stated climate objectives (EnerBlue), nuclear capacities would grow faster and reach 732 GW by 2050, while nuclear generation would reach 4,958 TWh. Under the most ambitious scenario, which would see the world align with the Paris Agreement objectives (EnerGreen), nuclear capacities would grow even faster and reach 840 GW by 2050, while nuclear generation would reach 5,608 TWh.

Figure 2: EnerFuture scenarios for the world's nuclear capacity and power production

Source:Enerdata, EnerFuture

Under every scenario, nuclear energy is expected to play a more critical role as the world transitions away from fossil fuels. These outlooks thus highlight the importance of the supply of enriched uranium, necessary to meet this anticipated growth in demand for nuclear power.

The basics of uranium enrichment

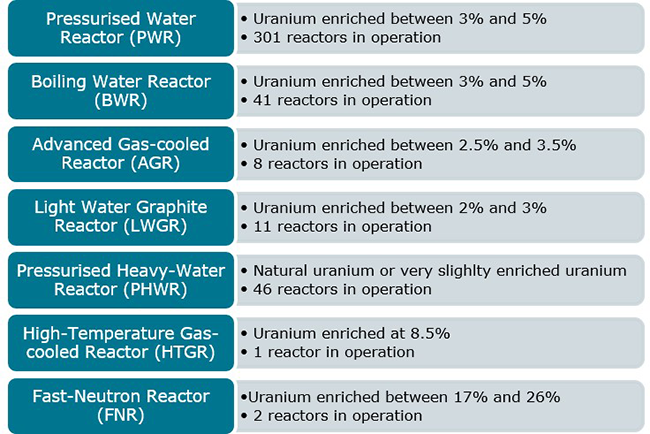

The rate of enrichment of uranium can be divided into four categories: slightly enriched uranium (SEU) between 0.9% and 3%, low enriched uranium (LEU) between 3% and 5%, high-assay low enriched uranium (HALEU) between 5% and 20%, and highly enriched uranium (HEU) at more than 20%. The 5% threshold was imposed in the standardisation of fuel manufacturing for pressurised water reactors, which represent most of reactors in service, although there is no technical justification for this limit. As for fuel for military use, the International Atomic Energy Agency (IAEA) sets the enrichment limit at 20%.

Enrichment consists in increasing the share of the uranium 235 isotope (235U) present in natural uranium (at about 0.7%). Natural uranium is previously converted into uranium hexafluoride (UF6), either by centrifugation or gas diffusion. In the case of centrifugation, a flow of UF6 passes through several centrifuges which will divide the UF6 into two flows: the first flow enriched in 235U and the second composed of depleted materials called “tails”. The effort required to separate these flows is quantified in Separative Work Units (SWUs).

Two strategies allow uranium refiners to achieve the expected concentration rates, depending on the availability of UF6 and SWUs.

- Underfeeding: For a given unit of enriched uranium, the operator reduces the volume of natural UF6 input, but increases the number of SWUs. This reduces the 235U concentration in the tails.

- Overfeeding: For the same unit of enriched uranium, the operator increases the volume of natural UF6 input and reduces the number of SWUs, but at the cost of a higher concentration of 235U in the tails.

There are different enrichment requirements, depending on the type of reactors currently in operation.

Figure 3: Enrichment rate for different reactor types (as of 2023)

Source: IRIS

How did Russia come to dominate the uranium enrichment sector?

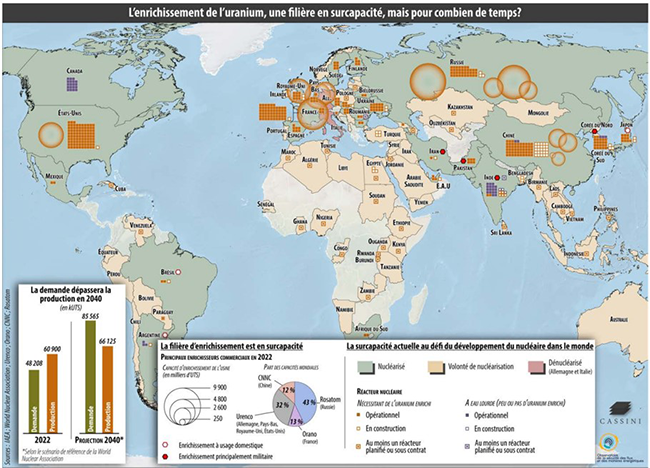

Globally, in 2022, the enrichment sector was in overcapacity and exceeded demand by 20%. However, this situation could change in the future. According to several scenarios2, current enrichment capacities will not be sufficient to cover demand by 2040 at the latest, due to a growth in demand mainly driven by Asia, and especially by China.

During the 2010s, the US’ share of enrichment capacities fell from 20% to 7.5%, due to a privatisation campaign launched in the 1970s and a gradual loss of competitiveness. This was accelerated by programs to dismantle Russian nuclear weapons, the warheads of which were used to produce enriched uranium for civilian use. This “Megatons to Megawatts” program flooded the American market with cheap enriched uranium.

Figure 4: Uranium enrichment, a sector in overcapacity, but for how long?

Source: Cassini

In Europe, Urenco, the continent’s main uranium player, has also seen its capacities reduced due to complex and divided governance over the future of the sector. France’s Orano is currently the sole European company working on a significant increase in its capacities, while Urenco plans to marginally develop its Eunice factory (located in the US).

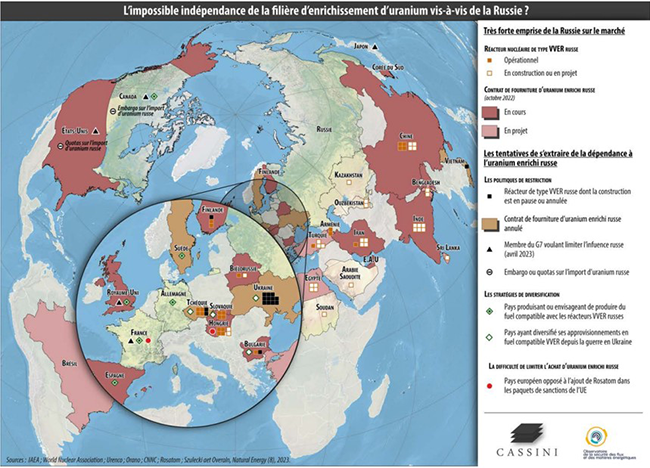

Simultaneously, Moscow launched with it state-owned company Rosatom a proactive commercial policy, relying on an offer integrating all the activities of the sector, taking advantage of prices among the lowest on the market and the support of the diplomatic services to circumvent regulatory barriers. This effort was successful, as Russia held 40% of the uranium enrichment market in 2023. It also provided 31% of the enrichment needs of European Union countries as well as 27% of the US’ demand in 2021.

This domination can be explained by a bloated production system, inherited from the Soviet Union, and by the fallout from the previously mentioned “Megatons to Megawatts” program, which allowed Russia’s capacities to be maintained after the fall of the USSR. The country currently has the capacity to meet 50% of global fuel demand, with the possibility of creating long-term dependence for countries wishing to equip themselves with Russian-designed nuclear capacity.

Figure 5: An impossible independence from Russia on the uranium enrichment sector

Source: Cassini

The impacts of the war in Ukraine on the sector

Uranium enrichment

The war in Ukraine has led to strong media coverage of the place taken by Russia on the enrichment market, with the fear of seeing Moscow use its dominant position for coercive purposes. Although this risk cannot be ruled out, it should nevertheless be moderated.

First, despite direct control from Moscow, Russian companies in the sector are financed mainly from their contracts abroad, limiting the financial influence of Russian power. Second, Russia has only marginal influence on material flows from Europe, North America, or Asia. Third, the significant energy density of enriched uranium allows operators to build up strategic stocks. Fourth, the share of enrichment in the production cost of a nuclear kWh remains low. Fifth, the export of fuel is a tool of soft power for the Kremlin, and a disruption in supply would seriously damage the image of Rosatom.

Despite this, Russia maintains control over Rosatom's strategic decisions and even a marginal increase in production costs in an already tight energy market remains risky. In the US, the Congress is working to define the framework for a gradual abandonment of imports of Russian 235U and the relaunch of national capacities for extraction, refining and enrichment of nuclear fuel on American soil. In Europe, divisions limit the action of the EU. Currently, the European strategy remains focused on the search for alternatives to Rosatom fuel in Russian-designed power plants holding VVER reactors.

Uranium transport

The transport of radioactive materials is more flexible than that of hydrocarbons, provided that it is equipped with dedicated packaging. The main constraint is compliance with international standards specific to radioactive materials, known as “class 7”.

In 2021, a quarter of the hundred largest ports in the world refused the loading, unloading or transit of class 7 materials, and only three shipowners took charge of part of radioactive materials (CMA-CGM, Hapag-Loys and Zim). These restrictions are explained by the compliance of port infrastructures to the political decisions of their public operator and by the logistical and financial constraints of managing small quantities of sensitive materials. In addition, the multiplication of takeovers of operators and shipowners by actors refusing the management of class 7 materials (notably due to fear of withdrawal from insurance companies) further limits flexibility. However, these elements do not constitute a risk of a complete breakdown in the supply of nuclear fuel. Nonetheless, they could force supply chain actors to move towards much more expensive charter alternatives.

The war in Ukraine has had no fundamental influence on the transport of enriched materials outside Russia, as Moscow has no control over transit between Europe or North America and alternative fuel suppliers. However, issues could arise concerning natural uranium from Central Asia and enriched in Russia. Historically, Kazakh and Uzbek uranium reached international markets through Russia, but due to the risks brought up by the current situation, the priority is starting to shift towards the development of alternative routes. The Trans-Caspian route, linking the port of Aktau in Kazakhstan to the Bosphorus Strait via Azerbaijan and Georgia, appears to be the preferred option, and despite logistical and regulatory limitations, it is on the verge of opening Central Asia to Western markets without going through Russia.

China is also developing alternative routes to import uranium from Kazakhstan to the Alashankou railway station (Xinjiang), which will be equipped in 2030 with a special purpose hangar able to hold the equivalent of Kazakhstan’s annual uranium production.

Saudi Arabia, China: future actors in the uranium enrichment market?

In January 2023, the Saudi Minister of Energy reiterated the Kingdom's intention to equip itself with the means of enriching uranium to ensure its complete independence in the production of nuclear fuel. In 2022, Riyadh launched its first call for tenders for the construction of two reactors in Khor Duweihin Bay. Enrichment is part of the strategy of indigenisation of the Saudi nuclear industry, taking advantage of uranium deposits identified in the country with the help of Chinese industrialists.

This choice is also made regarding the Iranian situation, which leaves doubt about the civilian nature of the Iranian program. The short-term development of Saudi enrichment capacity will have to involve either the import of centrifuges abroad or through technology transfer partnerships. Due to the conditions imposed by the US in terms of non-proliferation, Saudi Arabia could favour partnerships with less strict partners, first and foremost China.

In the medium term, centrifugation will remain the dominant enrichment technology. Six players are capable of manufacturing and assembling centrifuges at a commercial level: Enrichment Technology Company (ETC), a consortium between Orano and Urenco, the US’ Centrus, China’s CNNC, Rosatom, Japan’s JNFL and Brazil’s INB.

In the US, mastery of technology was gradually restricted to the military sector, but since 2019, an agreement between the American Department of Energy (DoE) and Centrus provides for the allocation of an AC-100M centrifuge for military use for the development of enriched uranium for civilian uses. In Europe, the reaction capabilities of the centrifuge industry are slower, as ETC's resources have decreased since 2003 and equipment modernisation projects risk being hampered by the loss of qualified labour.

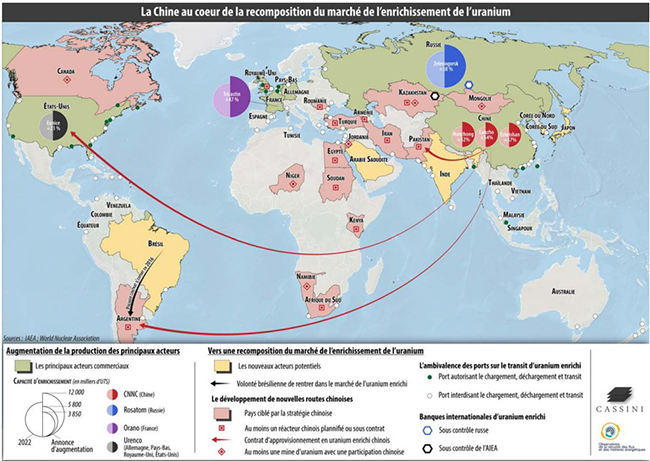

Unlike European and American actors, Rosatom has continually supplied orders to its centrifuge production industry. However, doubts persist about Russia's ability to nationally source all of the materials necessary to maintain its modernisation program. In China, CNNC is developing its capacity to export centrifuge enrichment services. In 2018, it announced the trial of a new generation of centrifuge with characteristics supposedly close to international standards.

Figure 6: China at the heart of the restructuring of the uranium enrichment market

Source: Cassini

The arrival of a new enricher into the centrifuge market would require one of these players to export its technologies. A possibility which cannot be ruled out in view of Rosatom's technological transfers and the shortcomings of the international non-proliferation regime.

Remaining challenges and solutions to mitigate the risks

New reactor models will require more enriched uranium

New reactor models requiring more enriched fuels are one of the main challenges in the evolution of the enrichment market. Of the 78 advanced reactor models listed in the AEIA ARIS database, 23 will require enrichment rates above 5%, of which 16 will be between 10% and 20% (HALEU). As for the US DoE, 22 of the designs selected for the Advanced Reactor Program require HALEU. The main advantage compared to LEU is to allow the use of smaller nuclear reactors as well as the extension of the duration between two reloadings.

The estimated future demand for HALEU is particularly uncertain but estimates from the Nuclear Energy Institute (NEI) predict a 150-fold increase in annual demand by 2035. However, there is currently no European or American enricher capable of meeting this request. The supply comes either from the decommissioning of US military uranium enriched to more than 20%, or from purchases from TENEX, Rosatom’s subsidiary for uranium enrichment.

In the US, no infrastructure has the capacity to support industrial demand for HALEU due to lack of authorisation. In Europe, there are no regulations authorising HALEU enrichment. On the other hand, the requested enrichment rates change from one reactor model to another, as does the form of the enriched uranium, with reactor manufacturers wishing to produce their own fuels. This lack of standardisation considerably complicates the control of the process and increases operating costs.

Since 2020, Washington has supported the availability of enriched uranium above 5% and below 20% for commercial use. The supporting measures taken in 2022 provide for the creation of a HALEU consortium, stimulation of demand, public funding, and adaptation of regulations. The European Union has, to date, no strategy for the development of a commercial HALEU sector. Only Great Britain is financing the development of HALEU production, transport and deconversion capacities.

What solutions to meet the projected need in more enriched uranium?

Due to the impossibility of rapidly increasing enrichment capacities, a temporary solution could be the rapid transition from an underfeeding enrichment situation to an overfeeding one. However, this would force the consumption of more natural uranium, even though this market is already affected by an increase in prices, which would shift existing tensions from enrichment towards uranium mining.

The main obstacle would come from the capacities to convert natural uranium into UF6, necessary before enrichment. The underfeeding which has dominated the market since the 2010s, as well as the dilution of military stocks have led to a reduction of conversion capacities. New conversion capacities are being developed (or reopened), but they are primarily intended to meet the increase in needs caused by the construction of new nuclear reactors and not for overfeeding.

In addition, the substitution of enriched uranium with MOX fuels using plutonium and depleted uranium cannot be achieved quickly, considering the lack of manufacturing plants and the low number of reactors authorised to use them. Likewise, the use of reprocessed uranium instead of natural uranium as an input resource will only make it possible to save very small volumes of enrichment.

CONCLUSION

The uranium enrichment sector was dominated by Russia well before its invasion of Ukraine, notably due to specific weapon dismantlement policies and a lack of competitiveness from the US and Europe. The war in Ukraine undoubtedly raised risks for the sector, such as a potential increase in production costs in an already tight energy market, but these risks must be moderated.

Indeed, Russia has very little control on flows outside its territory and Russian companies in the sector are financed mainly from their contracts abroad. Russia needs to keep this market running, as it is not only an important aspect of its economy, but also a tool of soft power for Moscow. In addition, the war in Ukraine has brought some major natural uranium producers, notably in Central Asia, to accelerate the development of alternate routes, bypassing Russian territory entirely.

However, the dominance of Russia on the uranium enrichment sector raises issues in the long-term. Russia currently has the capacity to meet 50% of global demand and Rosatom keeps pursuing modernisation programs, raising the risk of creating long-term dependence for countries wishing to equip themselves with Russian-designed nuclear capacity. As Russia dominates and the US and Europe lag behind, new actors could potentially emerge in the enrichment sector, notably China and Saudi Arabia.

Even though, globally, the enrichment sector is now in overcapacity and exceeds demand, current enrichment capacities will not be sufficient to cover needs by 2040 at the latest, due to a projected increase in demand. Indeed, new reactor models requiring more enriched fuels will become a major challenge for the enrichment market, as no country currently has the infrastructure to support the growing industrial demand for more enriched uranium. In addition, the lack of standardisation between countries complicates the control of the process and increases operating costs.

This Executive Brief stems from an analysis by Enerdata, the French Institute for International and Strategic Affairs (IRIS) and Cassini for the French Ministry of Defence (full report available in French here).

Notes

- World Energy Forecasts & Modelling | EnerFuture (enerdata.net)

- Notably from the World Nuclear Association, “Increase in SWU requirements by 2040 depending on the main nuclear development scenarios”.